Cheque printing & management software for India

Run the full life of a cheque in one place — a cheque-book register down to the individual leaf, printing onto your bank stationery, and a received → deposited → cleared/bounced lifecycle where clearing fires straight off your reconciled bank statement.

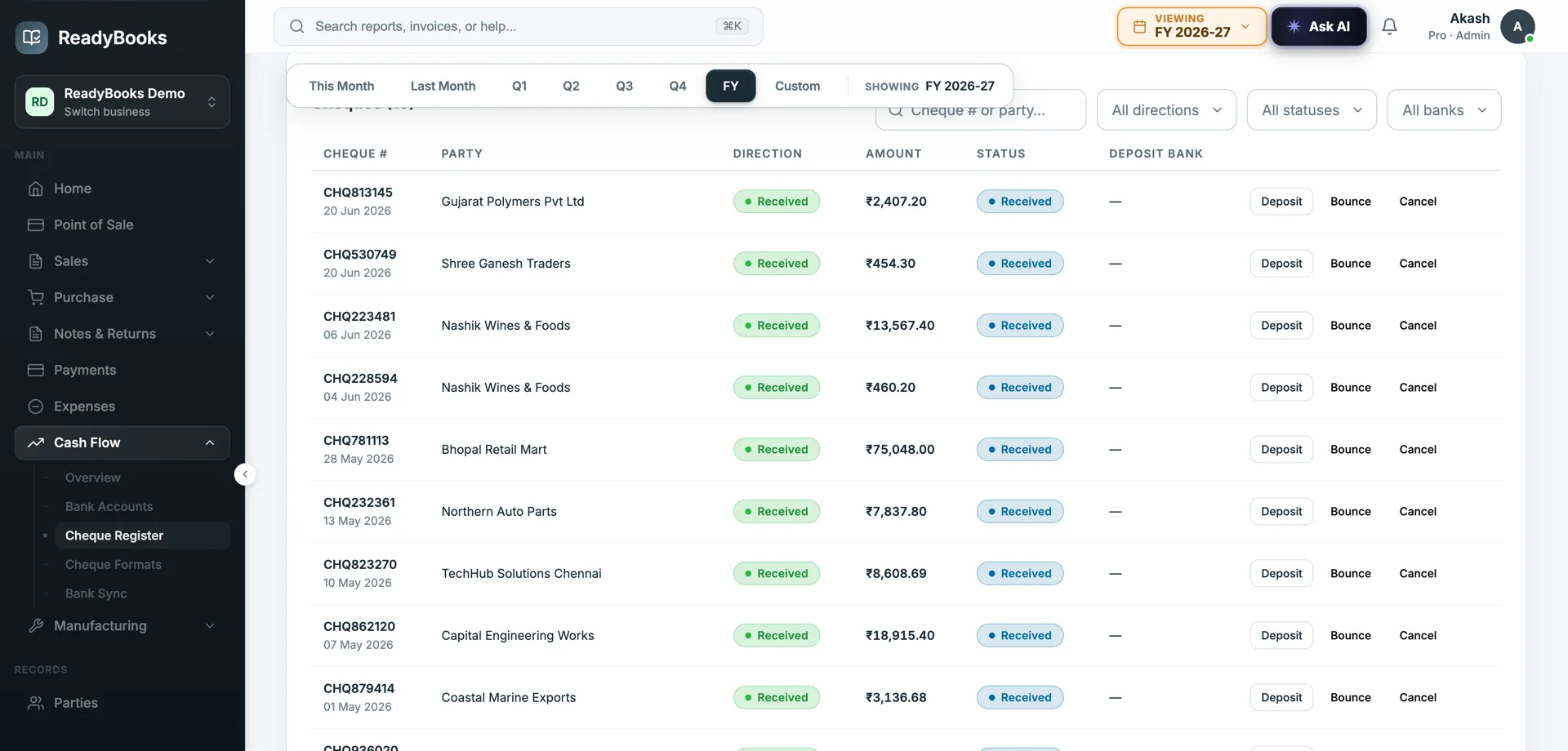

The cheque register — every received and issued cheque tracked through its lifecycle.

The whole cheque, issue to clearance

The physical leaf, the printed cheque, and the bank reconciliation stay in agreement — because they are one connected flow, not three screens.

The cheque-book register and cheque printing

Indian businesses still write a lot of cheques, and the bank stationery is numbered and finite. ReadyBooks treats that stationery as inventory you must account for.

A cheque book is registered by its leaf range, and from then on ReadyBooks tracks each leaf as its own object with a status: blank, issued, or cancelled. You can browse the register to see the whole book at a glance — which leaves remain, which were issued and against which payment, and which were cancelled. A spoiled leaf is cancelled rather than thrown away and forgotten, which is what keeps the numbering continuous and explainable; and if a leaf was cancelled in error, it can be restored. This per-leaf discipline is why the register can serve as a genuine control over your bank stationery instead of a rough list.

Printing is wired into the same register. ReadyBooks lays the payee name, the amount in both figures and words, and the date onto your bank’s pre-printed cheque using configurable print formats, so the fields fall into the correct positions for your specific bank’s layout. Crucially, printing a cheque draws the next available leaf from the book and marks it issued against the payment, so the physical cheque you just printed and the register entry can never tell two different stories about which leaf was used or what it paid.

Lifecycle, reconciliation-driven clearing, and bounces

A cheque is not cash until it clears. ReadyBooks models that explicitly and ties the moment of clearing to your real bank statement.

Every cheque you receive carries a status through its life: received when it comes in, deposited when you bank it, and then either cleared or bounced. Keeping these distinct matters for cash management — a deposited cheque is money you expect, not money you have, and ReadyBooks does not let it masquerade as available cash until it actually clears. At any time you can see the cheques still in hand, the cheques deposited and awaiting clearance, and the cheques that bounced and need chasing.

Clearing is deliberately conservative. The intended path is reconciliation-driven: while you reconcile a bank statement and confirm that a particular statement credit corresponds to a deposited cheque, ReadyBooks fires the clear-cheque action for you — and it routes through the same single, shared code path that a manual clear uses, so there is one definition of "cleared", not two that can drift. Because the trigger is a human-confirmed match against a real statement line, a cheque is never marked cleared on a hunch. When automation cannot help — no statement yet, or an unusual case — you can clear or bounce the cheque manually as a fallback.

Bounces are handled as first-class corrections. Marking a cheque bounced reverses the expected receipt so your books and cash position stop counting money that never arrived, and the customer’s balance reopens for follow-up or re-presentation. Every one of these transitions — deposit, clear, bounce, and any re-presentation — is recorded, so the history of a troublesome cheque is on the record rather than smoothed over. Pair this with full bank reconciliation and the cheque flow becomes the place where your book balance and your bank balance finally agree.

Where cheque control earns its keep

Three Indian scenarios where the register, the print run, and the bank must agree.