Credit note software built for Indian GST

Raise credit notes, debit notes, and sales returns that link straight to the original invoice or bill, reverse CGST, SGST, and IGST line by line, and flow into your GSTR-1 automatically. Every note posts its own double-entry journal and — for returns — restocks inventory, so a corrected sale stays in step with your books, your stock, and your filings.

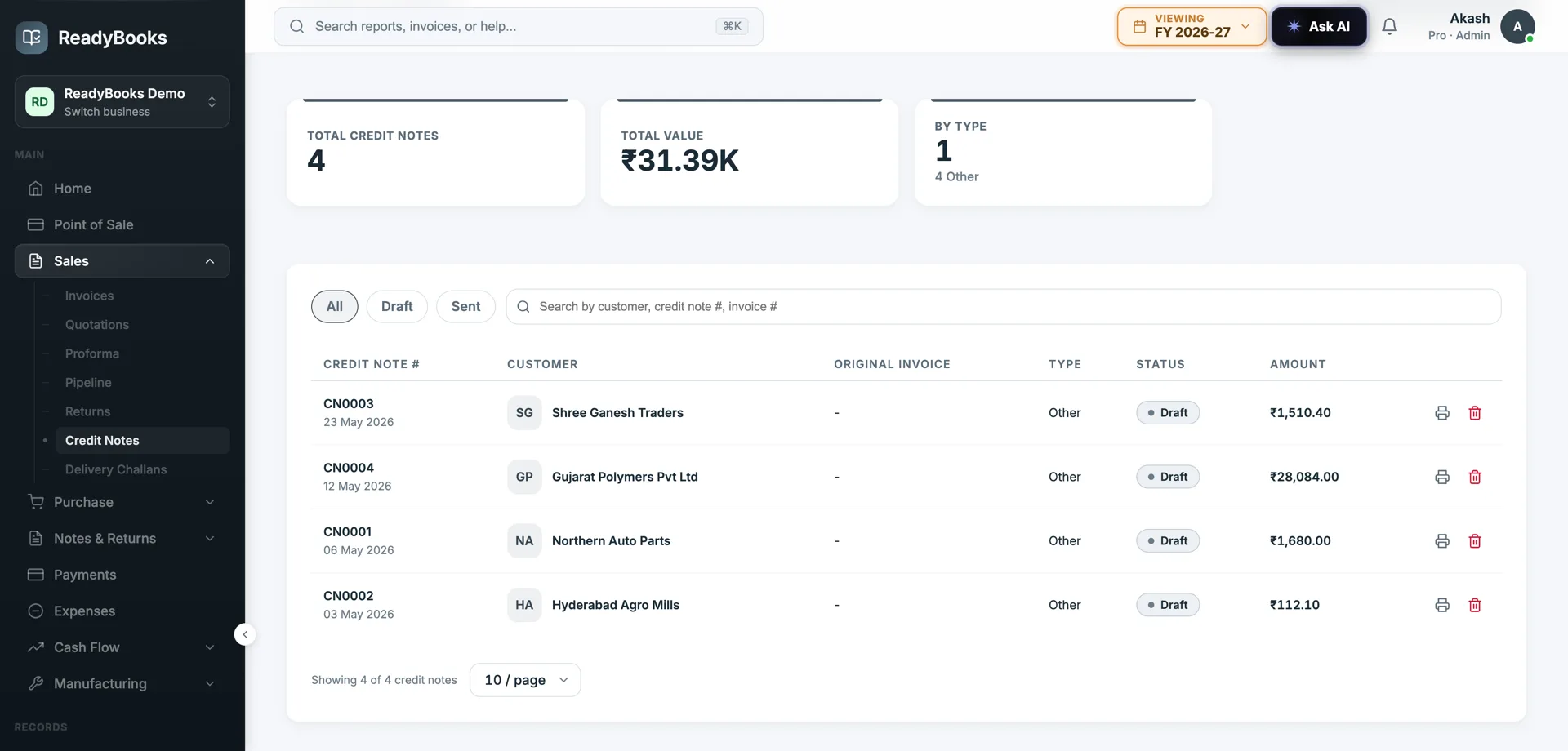

Credit notes linked to the parent invoice, with per-line GST reversal that feeds GSTR-1.

Every post-sale adjustment, done correctly

Credit notes, customer debit notes, sales returns, vendor debit notes, and vendor credit notes — each linked to its parent document and each posting the right GST and ledger entries.

GST credit notes and CGST/SGST/IGST reversal, explained

A credit note is the GST instrument for reducing the value of a tax invoice you have already raised. Done properly it reverses the exact output tax you charged — not an approximation.

Under GST, a registered seller issues a credit note when a tax invoice needs to be reduced after the fact: goods are returned, a post-sale discount is allowed, the rate or quantity was wrong, or the supply was deficient. The note must reduce the value and the tax originally charged. In ReadyBooks a credit note is created against its parent sales invoice and, where you want line-level precision, against the original invoice lines it adjusts. That linkage is not cosmetic — it is what lets the note inherit the original GST rate, the place of supply, and the HSN, so the reversal matches the supply it corrects.

Each credit note line carries its own CGST, SGST, and IGST columns, following the same intra-state versus inter-state determination as the original invoice. When you post the note, ReadyBooks writes a double-entry journal that reverses the output GST: it debits the CGST / SGST / IGST payable accounts for the tax portion and reduces the sale and the customer balance for the rest. Because the tax is reversed per line at the original rate, a partial return or a part-discount reverses exactly the proportionate tax — there is no single lump-sum tax figure to reconcile later.

A posted credit note also reduces the customer’s outstanding balance, so the next collection from that party already reflects the credit. Receivables, the GST output position, and the customer statement therefore stay consistent without you informally netting an amount off and losing the tax trail. The credit note carries the fields a GST credit note format needs — a unique number, the date, the original invoice reference, the taxable value, and the tax breakup — so the document you hand the customer is compliant and the same data drives your filing.

Sales return software: when the goods come back

A sales return is a distinct Indian document from a credit note. ReadyBooks keeps both because they do different jobs — one moves stock, the other moves money and GST.

When a customer physically returns goods, two things have to happen: the stock has to come back into your inventory at the right cost, and the customer’s liability and the output GST have to be reduced. ReadyBooks models the first with a sales return and the second with a credit note, so you can match your own workflow rather than forcing one document to do both. A sales return links to the original sales invoice and, line for line, to the original sale lines, so the system knows exactly what is coming back and against which sale.

The restock is valued correctly, not guessed. When you post a sales return, ReadyBooks looks up the unit cost of the original outward stock movement for that item and that invoice, and brings the returned quantity back in at that cost — falling back to the item’s weighted-average cost only when the original is unavailable. It then re-runs the full weighted-average-cost calculation across all movements for the item, on an advisory lock, so concurrent stock writers do not corrupt the cost basis. The result is that your on-hand quantity and your COGS are both correct after a return, not just your receivables.

The lifecycle protects the books. A sales return is a draft you can edit freely, it moves to sent when finalised, and posting it writes the stock movement and the journal entry. Editing or deleting a posted return reverses the prior stock movements before applying the new ones, so the inventory never double-counts a return. The financial reduction — the GST reversal and the cut to the customer balance — rides on the linked credit note, keeping the stock document and the money document cleanly separable for audit.

Debit notes, vendor adjustments, and the GSTR-1 feed

Adjustments cut both ways. ReadyBooks handles the purchase side with debit notes and vendor credit notes, and routes the outward documents into the correct GSTR-1 tables.

On the purchase side, when you return goods to a supplier or raise a claim against a bill, you create a debit note against the original purchase bill. It carries CGST, SGST, and IGST per line so the input tax credit you had claimed is reduced by exactly the right amount, and it reduces the payable balance you owe that supplier. The mirror document — a vendor credit note, which a supplier issues to you — is also a first-class record, so both halves of a purchase adjustment are captured against the right bill. As with sales-side notes, the parent-bill link keeps the GST rate and HSN correct and the audit trail intact.

The outward documents flow into GSTR-1 without re-entry. Credit notes you issue to customers feed the CDNR table for registered recipients and the CDNUR table for unregistered ones, while customer debit notes raised against a sales invoice feed the outward debit-note tables. The note number, the date, the original invoice it adjusts, the taxable value, and the CGST / SGST / IGST split all carry through from the document you raised — so the adjustments you made during the month land in the right GSTR-1 tables automatically. The purchase-side debit note is correctly treated as inward / ITC and is not pushed into your outward GSTR-1.

All of this sits inside one connected ledger, which is the point. A credit note reverses output GST and trims receivables; a sales return restocks inventory and re-bases cost; a vendor debit note reverses ITC and trims payables — each posting its own double-entry journal and each linked to its parent. You raise the documents in the natural course of business, and your books, your stock register, and your GST returns stay aligned without a separate reconciliation step. The same engine powers your invoicing, your purchases, and your GST compliance, so notes and returns are not a bolt-on but part of the spine.

Where notes & returns fit in your business

Three Indian scenarios the module is built for.